【保險】最新联邦法规对红蓝卡 D 部分做出了哪些重大强修调整? | BIEU LAM INSURANCE SERVICE | 林國彪保險

本纳税年度长者购买红蓝卡 D 部分处方药,个人自付的最高限额是多少?

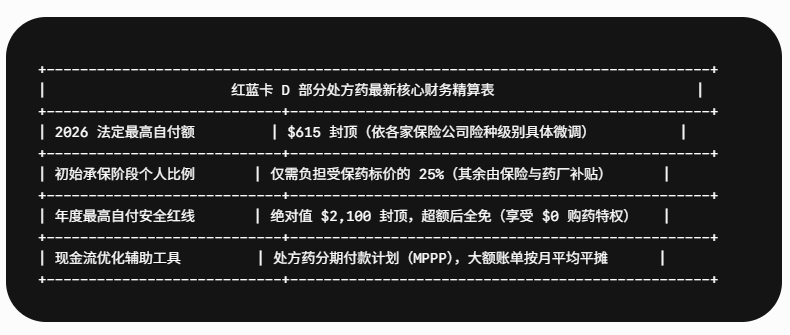

根据联邦医疗保险的最核心法定规范,长者购买红蓝卡 D部分(Part D)涵盖的处方药,其年度个人自付总额(Out-of-Pocket Maximum)被严格锁死在 $2,100。这意味着,一旦受益人全年在受保药物上的挂号费(Copay)和共同保险(Coinsurance)累计达到这一法定天花板,在接下来的整个日历年中,其购买所有受保药品的自付金额将直接归零($0)。

这一重大的消费者保护政策彻底终结了过去令无数华人家庭头疼的“甜甜圈洞”(Donut Hole)保障空窗期,极大降低了长期依赖昂贵慢性病特殊药物长者的财务负担。然而,若想在日常生活中实现资金最大化对冲,企业主和高净值家庭仍需牢记以下最新精算指标:

- 法定制药自付额上限: 本年度任何独立处方药险或含药优势计划,其设定的处方药年度初始自付额(Deductible)最高不得超过 $615。部分高端保单会对普通通用型仿制药(Generic)直接豁免该自付额。

- 25% 标准初始自付期: 在扣除自付额后、达到 $2,100 自付封顶线之前,投保人通常需承担药费总额的 25% 作为标准共同保险。

- 分期平滑分摊机制: 联邦政府全面推行了“红蓝卡处方药分期付款计划”(MPPP),长者可向承保公司申请将年初高昂的药费支出平均分摊到全年各个月份中,变成可预测的小额月缴,从而极大地优化家庭资金周转。

这一年度自付额封顶政策是否适用于保险公司目录外的所有药物?

不适用。该项年度 $2,100 的个人自付封顶红利,严格且仅适用于您所投保的特定保险计划官方“处方药报销目录”(Formulary)内的药品。如果长者购买了目录外的非受保药物,或违反了承保公司的处方规范,除非通过资深顾问协助成功申请并获批“目录例外豁免”(Formulary Exception),否则相关开支将无法计入这 $2,100 的安全防线中。

在加州本地,年长者应如何运用策略进一步拉低药费成本?

什么是“优选药局网络”与“药物分级”?它们如何影响我的买药成本?

优选药局网络(Preferred Pharmacy Network)与药物分级(Formulary Tiers)是通过精细化就医行为来降低自付额的决定性机制。投保人如果选择在保险公司指定的“优选成本分摊药局”配药,其挂号费或共同保险比例会远低于普通的网络内药局;同时,全面选用处于 Tier 1 或 Tier 2 级别的低成本仿制药,能极大地延缓甚至免除触及自付额的过程。

对于南加州華人居住區域,羅蘭崗及阿卡迪亚及圣盖博谷周边的华裔社群而言,由于每家商业保险公司(如 Anthem、Blue Shield 等)每年都会根据加州保险局(CDI)的最新精算报告,重新调整其药物报销分级以及合作药局名单。这意味着,去年最便宜的保单,今年很可能因为某个核心药物品级的调高或药局合作的终止,导致自付费用飙升。林标保险的个人风险管理专家团队会利用智能精算系统,将您现有的日常用药清单与本年度各大主流计划的最新名录进行精准交叉比对。我们绝不使用恐吓营销,而是以透明的技术参数为您筛选出最具性价比的 D部分组合,最大化扣减您的日常摩擦开支,确保您的财富与健康立于坚实长青的基石之上。

有需要任何建議諮詢,請聯繫林國彪保險Bieu Lam Insurance 。我們另外有福地墓園,殯儀服務一站式協助。

免責聲明:本文內容僅供教育與資訊參考之用。保險政策條款、承保範圍及符合資格之要求可能會有所變動。具體的健康保險承保內容及保費補助資格,須以保險公司核保結果、收入審查及實際保險合同條款為準。

Part D Savings: How to Lower Your Prescription Drug Costs This Year

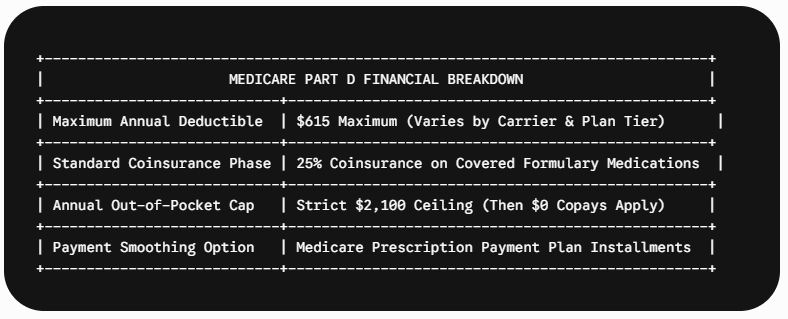

Under the latest federal guidelines, a senior's maximum out-of-pocket cost for covered Medicare Part D prescription drugs is capped at exactly $2,100 per calendar year. Once a beneficiary's out-of-pocket spending reaches this mandatory threshold, they are legally exempt from paying any copayments or coinsurance for covered formulary medications for the remainder of the plan year.

This consumer protection entirely eliminates the historically problematic "donut hole" coverage gap, providing significant financial relief for local seniors managing multiple chronic diagnoses. However, navigating your specific plan's design still requires evaluating key underlying statutory parameters:

- The 2026 Deductible Cap: The maximum standard annual deductible that any Part D or Medicare Advantage prescription drug plan can charge is $615. Some premier regional plans may feature lower or waived deductibles for generic tiers.

- The 25% Initial Coinsurance: After meeting your plan's deductible, you are generally responsible for a standard 25% coinsurance of the retail drug cost until you hit the definitive $2,100 out-of-pocket limit.

- The Prescription Payment Plan: Beneficiaries can opt into the federal Medicare Prescription Payment Plan, an installment program that allows you to smooth out high upfront out-of-pocket pharmacy bills into predictable monthly payments throughout the remaining months of the year.

Does the annual cap apply to medications that are not on my plan's formulary?

No, the annual out-of-pocket cap applies exclusively to medications that are explicitly listed on your specific insurance plan's approved formulary. If you purchase a drug that is excluded from the plan's drug list, or if it is deemed non-covered by underwriter guidelines, those costs will not count toward the annual cap unless an official formulary exception is formally granted.

How Can Seniors Strategically Lower Pharmacy Costs in California?

How do preferred networks and formulary tiers affect my prescription drug costs?

Preferred pharmacy networks and formulary tier placements affect your prescription drug costs by dictating the exact copayment or coinsurance percentage assigned to each medication. Sourcing your maintenance prescriptions from an insurance carrier's designated "preferred cost-sharing" pharmacies, rather than standard in-network pharmacies, significantly reduces your daily expenses and preserves your out-of-pocket capital.

For families and business owners in Southern California hubs like Arcadia and the San Gabriel Valley, executing a targeted annual formulary audit is essential to avoid unnecessary premium drag. Medications are strictly categorized into tiers, ranging from low-cost preferred generics to high-cost specialty biologics. Because individual private carriers modify their tiered assignments and preferred pharmacy alliances every single year, a plan that was highly efficient previously may become non-optimized now. Our proactive personal risk management specialists utilize advanced comparative technology to map your current prescriptions against active regional underwriting directories, ensuring you secure the highest savings available under California Department of Insurance (CDI) frameworks.

图片翻摄自网路,版权归原作者所有。如有侵权请联系我们,我们将及时处理。